The Energy Consulting Group

Business strategy for upstream oil and gas producers and service companies

Mexico

|

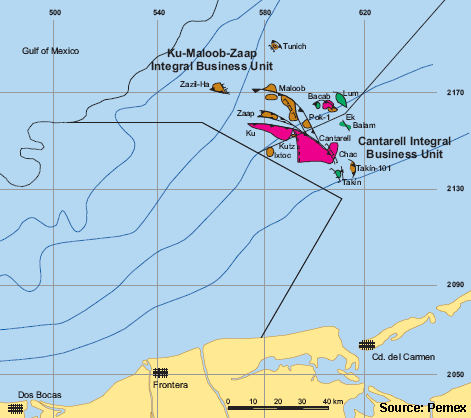

Oil and Gas Industry Overview Map of Mexico Click on image for higher resolution image. Map contains approximate locations in Mexico for oil fields, natural gas fields, oil pipelines, natural gas pipelines, existing natural gas fired power plants, potential natural gas fired power plants, LNG import terminals, and oil export terminals. |

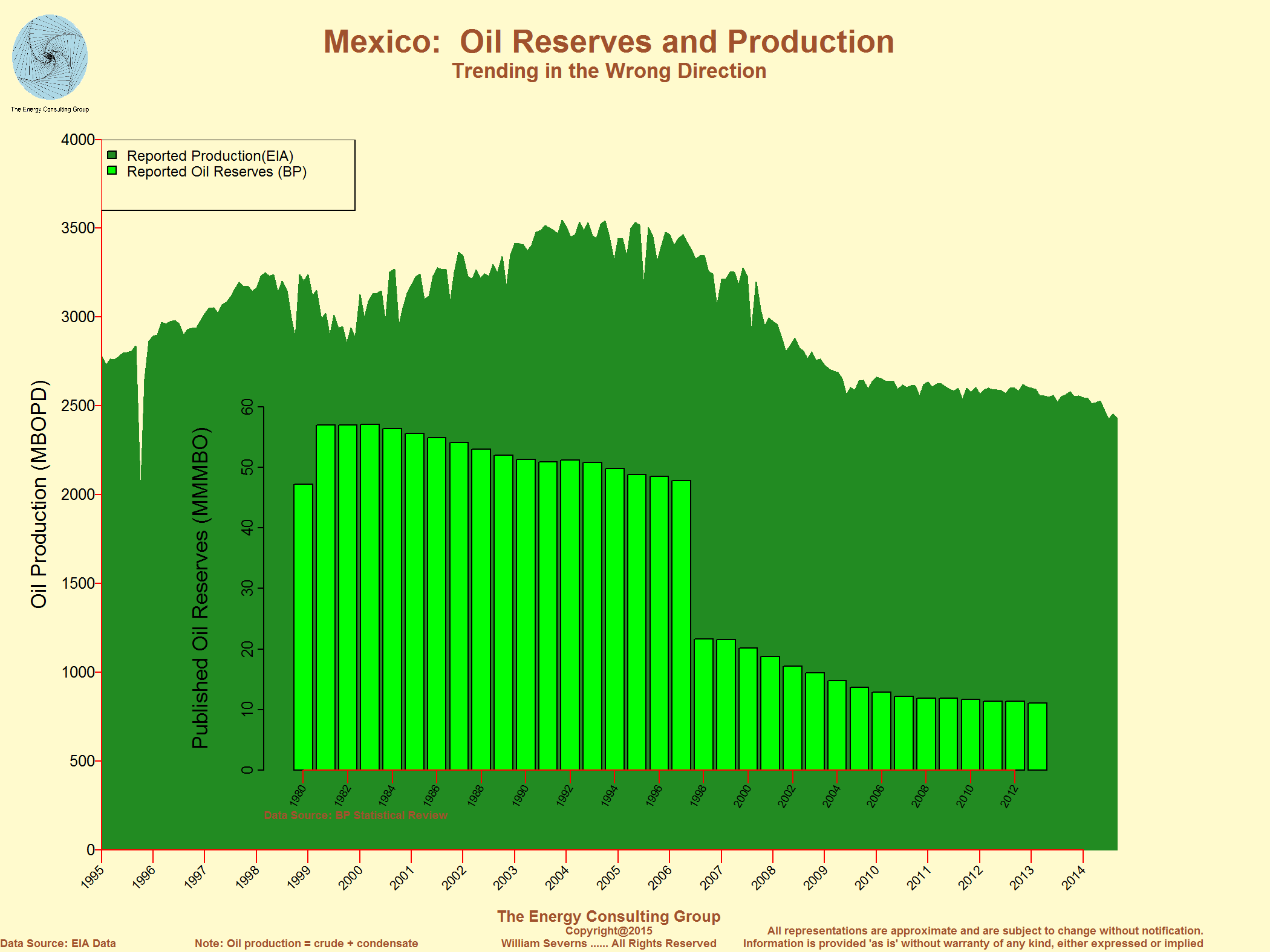

Chart of Oil Production and Oil Reserves for Mexico Click on image for higher resolution image.

Click on image for higher resolution image. |

====================================================================================================================================================

Mexico: Country Overview

(source: EIA)

Overview

Mexico is a major non-OPEC oil producer and is among the largest sources of U.S. oil imports.

Mexico is one of the 10 largest oil producers in the world, the third-largest in the Americas after the United States and Canada, and an important partner in the U.S. energy trade. However, Mexico's oil production has steadily decreased since 2005 as a result of natural production declines from Cantarell and other large offshore fields. The rate of total production decline has abated in past several years. In December 2013, in an effort to address the declines of its domestic oil production, the Mexican government enacted constitutional reforms that ended the 75-year monopoly of Petroleós Mexicanos (PEMEX), the state-owned oil company.

Oil is a crucial component of Mexico's economy. The oil sector generated 13% of the country's export earnings in 2013, a proportion that has declined over the past decade, according to Mexico's central bank. More significantly, earnings from the oil industry (including taxes and direct payments from PEMEX) accounted for about 32% of total government revenues in 2013. Declines in oil production have a direct impact on the country's economic output and on the government's fiscal health, particularly as refined product consumption and import needs grow.

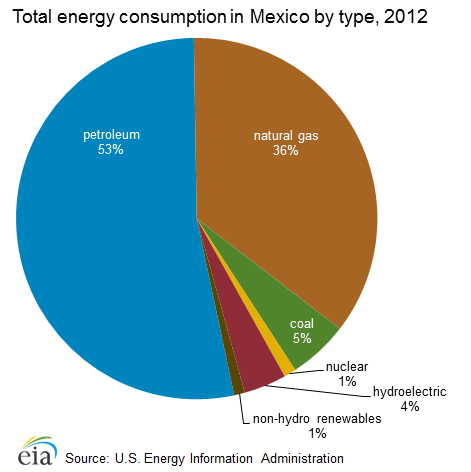

Mexico's total energy consumption in 2012 consisted mostly of oil (53%), followed by natural gas (36%). Natural gas is increasingly replacing oil as a feedstock in power generation. However, because Mexico is a net importer of natural gas, higher levels of natural gas consumption will likely depend on more pipeline imports from the United States or liquefied natural gas (LNG) imports from other countries. All other fuel types contribute relatively small amounts to Mexico's overall energy mix. Most of Mexico's non-hydro renewables consumption is attributable to traditional biomass, the use of which is important in rural areas. The country also has noteworthy geothermal and wind energy sectors.

Source: CIA World Factbook

Oil

Mexico's oil production has declined in recent years, as has its position as a net oil exporter to the United States.

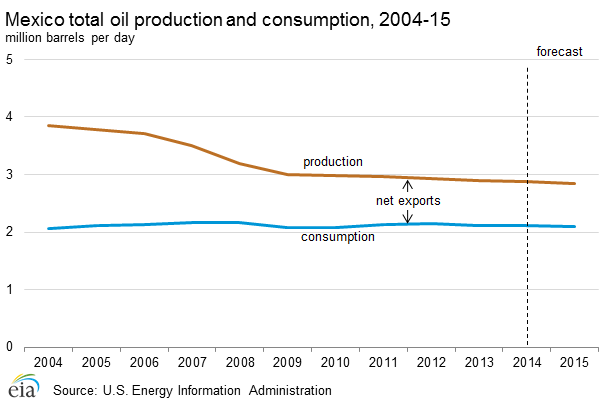

Mexico produced an average of 2.9 million barrels per day (bbl/d) of total oil liquids during 2013. Crude oil accounted for 2.5 million bbl/d, or 87% of total output, with the remainder attributable to lease condensate, natural gas liquids, and refinery processing gain. Mexico's total oil production had been declining substantially, 22% from its height in 2004 to 2009, but the decline thereafter has remained at less than 1% per year. Notably, crude oil production in 2013 was at its lowest since 1995 and continues to decline thus far in 2014. Mexico is a significant, third largest in the Americas, but declining net crude exporter, and the country is a net importer of refined petroleum products. Its largest trading partner is the United States, which is the destination for most of its crude oil exports and the source of most of its refined product imports. More information on Mexico's oil production in the context of production in the Americas can be found in the recent EIA report on Liquid Fuels and Natural Gas in the Americas.

Reserves

According to the Oil & Gas Journal (OGJ), Mexico had 10 billion barrels of proved oil reserves as of the end of 2013. Most reserves consist of heavy crude oil varieties, with the largest concentration occurring offshore of the southern part of the country, particularly the Campeche Basin. There are also sizable reserves in onshore basins in the northern parts of the country.

Sector organization

Mexico nationalized its oil sector in 1938, and PEMEX was created as the sole oil operator in the country. PEMEX is the largest company in Mexico and one of the largest oil companies in the world. The energy sector is regulated by the Secretaría de Energía (SENER) and the Comisión Nacional de Hidrocarburos (CNH) provides additional oversight of PEMEX and its oil and gas activities.

After years of declining production, Mexico instituted its most significant energy reforms to date. In December 2013, the Mexican government enacted constitutional reforms ending PEMEX's monopoly on the oil and gas sector and opening it to greater foreign investment. The reforms allow for new exploration and production contract models: licenses, production-sharing, profit-sharing, and service contracts. Previously, only service contracts, in which companies were paid for services and were not allowed shares or profits derived from the hydrocarbon resources, were allowed for foreign firms. PEMEX will remain state-owned but will be given more budgetary and administrative autonomy and will have to compete for bids with other firms on new projects. The reforms also call for expanding the regulatory authorities to SENER, CNH, and for creating a new National Agency of Industrial Safety and Environmental Protection. As stipulated by the reforms, PEMEX was allowed first refusal of its current oil and gas holdings and has submitted to the energy ministry its desire to retain and develop deepwater oil fields in the Perdido Fold Belt and offshore Lakach gas fields.

Mexico must now develop and approve secondary legislation detailing the fiscal regime and contract terms for the models. While reform proponents overcame the major obstacle of constitutional change, the remaining legislation still faces significant opposition. Mexico's government plans to offer acreage for bidding that is open to international firms by 2016-17.

Exploration and production

Most of Mexico's oil production occurs off the eastern coast in the Bay of Campeche of the Gulf of Mexico, near the states of Veracruz, Tabasco, and Campeche. The two main production centers in the area are Cantarell and Ku-Maloob-Zaap (KMZ). In total, approximately 1.9 million bbl/d — or three-quarters — of Mexico's crude oil is produced offshore in the Bay of Campeche. Because of the concentration of Mexico's oil production offshore, tropical storms or hurricanes passing through the area can disrupt oil operations.

OffshoreOver half of Mexico's oil production comes from two offshore fields in the northeastern region of the Bay of Campeche--Ku-Maloob-Zaap (KMZ) and Cantarell. Another important source of oil production is southwest in the same bay, offshore Tabasco state. Most of the oil produced at KMZ and Cantarell is heavy and marketed as Maya blend, while the oil produced offshore Tabasco is a lighter grade.

Cantarell was once one of the largest oil fields in the world, but its output has been declining significantly for almost a decade. Production at Cantarell began in 1979, but stagnated as a result of falling reservoir pressure. In 1997, PEMEX developed a plan to reverse the field's decline by injecting nitrogen into the reservoir to maintain pressure, which was successful for a few years. However, production resumed a rapid decline beginning in the middle of the last decade—initially at extremely rapid rates, and more gradually in recent years. In 2013, Cantarell produced 440,000 bbl/d of crude oil, which was nearly 80% below the peak production level of 2.1 million bbl/d reached in 2004. As production at the field has declined, so has its relative contribution to Mexico's oil sector. Cantarell accounted for 17% of Mexico's total crude oil production in 2013, compared with 63% in 2004.

Meanwhile, KMZ, which is adjacent to Cantarell, has emerged as Mexico's most prolific field. Production nearly tripled between 2004 and 2013, when it reached 864,000 bbl/d, as PEMEX used a nitrogen reinjection program similar to that used at Cantarell. PEMEX hopes to increase output further over the next few years, in part through the development of the anticipated 100,000-bbl/d Ayatsil satellite field, although views differ about whether the KMZ complex has already reached peak production.

Mexico's other offshore oil production center is to the southwest in the Bay of Campeche, near the state of Tabasco. There the Abkatun-Pol-Chuc and Litoral de Tabasco projects, each consisting of several small fields, accounted for a combined 593,000 bbl/d of oil production in 2013. The production trajectories of the two field complexes differ considerably. Output from Litoral de Tabasco has increased from less than 200,000 bbl/d in 2008 to nearly 300,000 bbl/d in 2013, offsetting some of the declines at Cantarell. Litoral de Tabasco also includes the promising Tsimin and Xux discoveries. Production from Abkatun-Pol-Chuc, on the other hand, has declined considerably from peak levels achieved in the mid-1990s, when output exceeded 700,000 bbl/d; production in 2013 was under 300,000 bbl/d.

Mexico is believed to possess considerable hydrocarbon resources in the deepwater Gulf of Mexico that have not yet been developed. PEMEX has been drilling deepwater exploratory wells since 2006, making its first significant find in the Perdido Fold Belt, near the U.S. maritime border, in August 2012. In February 2012, the United States and Mexico signed a Transboundary Hydrocarbon Agreement concerning the development of oil and gas reservoirs that extend across their maritime border. The agreement established a cooperative process and legal framework for safely managing and jointly utilizing transboundary reserves, and ends the current moratorium on exploration and production in the transboundary area. Furthermore, in March 2014, as part of the newly-enacted energy reforms, PEMEX submitted its request to maintain and develop those fields in the Perdido Fold before Mexico opens undeveloped fields to international investors.

OnshoreOnshore fields accounted for 25% of Mexico's total crude oil production in 2013. Most of this production consists of light or extra-light crude oil in the southern part of the country, accounting for 77% of Mexico's onshore production. The largest oilfield in the south is Samaria-Luna, which produced about 173,000 bbl/d in 2013.

The most notable onshore prospect in the north is the Aceite Terciario del Golfo (ATG) project, better known as Chicontepec, which is located northeast of Mexico City. PEMEX has heavily invested in and promoted Chicontepec as a potentially significant source of future production, with 637 million barrels of proved crude oil reserves and 15 billion more barrels of probable and possible reserves.

Despite its potential, production in Chicontepec averaged only 66,000 bbl/d in 2013, a decline from 2012. Chicontepec has not lived up to expectations because of the unique technical challenges associated with its development. In fact, Chicontepec is not a single field but a formation with dozens of small fields spread over hundreds of square miles, which are highly fractured and at low pressure. As a result, many costly development wells are necessary, recovery rates are low, and decline rates are high. Moreover, the region does not yet have much of the supporting infrastructure necessary for large-scale oil development. PEMEX hopes to significantly increase production through an aggressive drilling program, aspiring to produce 300,000 bbl/d from Chicontepec by the next decade. However, many industry analysts expect production to peak far earlier, and at a much lower level, without significant foreign investment. Mexico's energy regulator, CNH, has raised concerns about the project's profitability and PEMEX's development plan, given that Chicontepec accounts for a significant share of the company's exploration and production budget.

Source: PEMEX

Trade

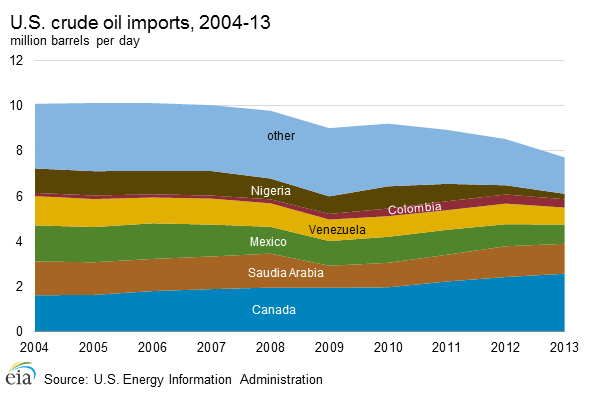

Mexican authorities report that the country exported 1.19 million bbl/d of crude oil in 2013, a decline that has occurred since 2010. The United States received approximately 71% of Mexico's oil exports, which arrived by tanker. Most Mexican crude oil exports to the United States are Maya blend, while Mexico retains most of the output from its lighter crude streams—Isthmus and Olmeca—for domestic consumption. The United States will continue to attract the bulk of Mexico's oil exports because of the proximity and the operation of sophisticated U.S Gulf Coast refineries capable of processing heavier Maya crudes.

Mexico is typically among the top three exporters of oil to the United States. In 2013, the United States imported 850,000 bbl/d of crude oil from Mexico, behind Canada and Saudi Arabia. Mexico's crude oil exports to the United States rose steadily through the 1980s and 1990s, before peaking in 2004 at 1.6 million bbl/d. U.S. crude oil imports from Mexico have generally declined since 2006, reflecting the Mexico's steady drop in crude oil production and rising fuel demand, and other developments related to U.S. supply.

Petroleum products exports and importsDespite its status as a large crude oil exporter, Mexico is a net importer of refined petroleum products. According to PEMEX, Mexico imported 603,000 bbl/d of refined petroleum products in 2013, of which 60% was gasoline and most of the remainder was diesel and liquefied petroleum gases (LPG). Mexico was the destination for 44% of U.S. exports of motor gasoline in 2013, although imports from the United States have declined since 2011.

In 2013, Mexico exported 182,000 bbl/d of refined petroleum products. The United States imported 68,000 bbl/d of that total, most of which was residual fuel oil, naphtha, and pentanes plus. As with crude oil, U.S. imports of refined petroleum products from Mexico have declined in recent years, from a high of 132,000 bbl/d in 2010.

Pipelines and export terminals

PEMEX operates an extensive pipeline network in Mexico that connects major production centers with domestic refineries and export terminals. According to PEMEX, this network consists of pipelines spanning over 3,000 miles, with the largest concentration occurring in southern Mexico.

Theft of oil from pipelines has become increasingly problematic in Mexico. Organized crime groups and armed gangs, some believed to have ties to drug cartels, and they control areas transited by pipelines and fuel trucks from which oil is taken. The scale of the problem is uncertain, and estimates of the stolen oil vary, but Mexican officials have declared that between 2012 and 2013 over 1,500 illegal fuel taps caused about $1.1 billion in losses. Sinaloa and Veracruz have been cited as the most affected states in recent years.

Mexico has no international oil pipeline connections. Most of its exports are shipped by tanker from three export terminals on the Gulf Coast in the southern part of the country: Cayo Arcas, Dos Bocas, and the Pajaritos terminal at the port of Coatzacoalcos. There is also an export terminal on the Pacific Coast at Salina Cruz.

Downstream

Mexico's total oil consumption remained relatively steady over the past five years, and averaged 2.1 million bbl/d in 2013. According to Mexican government data, gasoline accounts for roughly 44% of the country's petroleum product sales and diesel for another 29%.

Mexico has six refineries, all operated by PEMEX, with a total refining capacity of 1.54 million bbl/d as of the end of 2013. According to PEMEX, actual refinery output was 1.46 million bbl/d in 2013, below capacity but an increase after two consecutive years of decline. PEMEX also controls 50%of the 334,000-bbl/d Deer Park refinery in Texas.

Mexico plans to reduce its imports of refined products by improving domestic refinery capacity. In February 2012, PEMEX awarded a contract for the design of a new 300,000 bbl/d facility at Tula. While intended to be operational by 2016, it has already experienced delays. The Tula plant would be the first new refinery built in Mexico in 30 years. An expansion of the Minatitlan refinery, completed in early 2012, will increase production of diesel and gasoline by 34,000 bbl/d and 47,000 bbl/d, respectively. Despite these developments, industry analysts contend that Mexico does not have a natural competitive advantage in refining, given the country's close proximity to a sophisticated U.S. refining center. Some feel that it would be more productive to apply PEMEX's limited capital to the upstream sector.

Natural gas

Mexico is a net importer of natural gas, mostly via pipeline from the United States, and its natural gas demand is rising because of greater use for power generation.

Mexico has considerable natural gas resources, but its production is modest relative to other North American countries (See Liquid Fuels and Natural Gas in the Americas). The development of its shale gas resources is proceeding slowly. Mexico's import needs are rising as domestic production stagnates and demand increases, particularly in the electricity sector. Consequently, Mexico will rely on increased pipeline imports of natural gas from the United States and liquefied natural gas (LNG) from other countries.

Reserves

According to OGJ, Mexico had 17 trillion cubic feet (Tcf) of proved natural gas reserves at year-end 2013. While the southern region of the country contains the largest share of proved reserves, the northern region has the potential to be the center of growth in future reserves, as it contains almost 10 times as much probable and possible natural gas reserves.

Mexico has one of the world's largest shale gas resource bases, which could support increased natural gas reserves and production. According to the U.S. Energy Information Administration's (EIA) assessment of world shale gas resources, Mexico has an estimated 545 Tcf of technically recoverable shale gas resources–the sixth largest of any country examined in the study. The figure of technically recoverable shale gas resources is far smaller than the total resource base because of the geologic complexity and discontinuity of Mexico's onshore shale zone, and other issues, including the availability of required technology and water resources are more pessimistic about the country's true potential. Most of Mexico's shale gas resources are in the northeast and east-central regions of the country. The Burgos Basin, which accounts for the majority of Mexico's technically recoverable shale gas resources, parts of the Eagle Ford shale play, considered to be Mexico's most promising prospect and a prolific source of natural gas production in Texas.

Source: World Shale Gas and Shale Oil Resource Assessment, U.S. Energy Information Administration

Sector organization

Before the energy reforms of 2013, PEMEX retained a monopoly on natural gas exploration, but the government allowed private participation in non-associated gas exploration and production. The Mexican government opened the downstream natural gas sector to private operators in 1995, although no single company may participate in more than one downstream function (transportation, storage, or distribution). The Comisión Reguladora de Energía (CRE) was created to monitor the sector.

As it applies to the oil sector, the newly-enacted energy reforms allow for greater outside investment into exploration, production, and other activities in the gas sector. The reforms allow for new exploration and production contract models: licenses, production-sharing, profit-sharing, and service contracts. PEMEX will remain state-owned but will be given more budgetary and administrative autonomy and will have to compete for bids with other firms on new projects. The reforms also call for expanding the regulatory authorities to SENER, CNH, and a create new National Agency of Industrial Safety and Environmental Protection. As stipulated by the reforms, PEMEX was allowed first refusal of its current oil and gas holdings and has submitted to the energy ministry its desire to retain and develop deep water oil fields in the Perdido Fold Belt and Lakach gas fields.

Exploration and production

Mexico produced an estimated 1.7 Tcf of dry natural gas in 2012, a modest decline from the year before. Part of the decline is due to a divergence in the prices for natural gas and crude oil, which encouraged PEMEX to favor exploitation of oil.

CNH reports that approximately 153 million cubic feet per day of natural gas was vented and flared in 2013, just under 20% of which occurred at Cantarell. PEMEX and government agencies have prioritized a reduction in gas flaring for economic and environmental reasons. Efforts to improve the infrastructural capacity to capture, process, and transport associated natural gas production, particularly at Cantarell, have been effective and gas utilization rates have recently increased.

The geographic distribution of Mexico's marketed natural gas production is slightly different and more dispersed than it is for oil. According to statistics from Mexico's CNH, more than two-thirds of Mexico's natural gas production in 2013 was from associated oil fields. Unlike in the oil sector, the onshore (Samaria-Luna) and offshore fields of Tabasco yield more natural gas than Cantarell or KMZ. Over two-thirds of the country's non-associated natural gas production occurred in the Burgos Basin in the northern part of the country; most of the remainder was from nonassociated fields in Veracruz.

Mexico has taken preliminary steps to explore for and produce shale gas, but lags the United States considerably in terms of the development of its shale gas and tight oil potential. PEMEX produced its first shale gas in early 2011 from an exploratory well in northern Mexico. Later that year, the government announced a significant discovery in the same region, which could significantly increase the country's proven natural gas reserves. PEMEX announced in early 2014 that it planned on drilling 10 shale test wells, bringing Mexico's total to 175, a small figure compared with the more than 13,000 wells drilled across the border in Texas. While PEMEX has allocated a small share of its budget to shale gas development, the sector is unlikely to grow rapidly without improvement in PEMEX's financial situation, technical abilities, and terms for investors. However, the pending finalization of energy reforms could bring in foreign firms to accelerate development of Mexico's shale gas resources.

Trade

Mexico is a net importer of natural gas, with most imports arriving via pipeline from the United States. Mexico imported a total of 779 Bcf of natural gas; 620 Bcf came from the United States in 2012. As U.S. shale gas output boomed, North American natural gas prices fell, and Mexico's consumption needs further exceeded its productive capacity. U.S. natural gas exports to Mexico accounted for over 38% of total U.S. natural gas exports, and nearly 80% of Mexico's natural gas imports. The United States imports a small amount of natural gas from Mexico, and the trade imbalance is expected to increase even further as recent supply and demand trends in both countries are projected to continue.

Liquefied natural gas (LNG)Mexico meets some of its natural gas demand with LNG. According to the International Energy Agency (IEA), Mexico imported roughly 224 Bcf of LNG in 2012, of which 40% came from Qatar, 22% from Nigeria, and 15% from Peru, with smaller volumes from Indonesia and other countries. Mexico's LNG supply mix has changed in recent years, as increased volumes from Qatar displaced LNG from Egypt, Trinidad and Tobago, and most notably Nigeria, which had been Mexico's largest source of LNG.

PipelinesAccording to PEMEX, the company operates over 7,400 miles of natural gas pipelines in Mexico. The company has 11 natural gas processing centers with 69 natural gas processing plants. PEMEX operates most of the country's natural gas distribution network, which supplies processed natural gas to consumption centers. The natural gas pipeline network includes 13 operational interconnections with the United States, and at least 2 new pipeline interconnections are planned to supply the growth in Mexico's natural gas demand.

Electricity

Most of Mexico's electricity generation comes from fossil-fueled power plants, which increasingly use natural gas as a fuel source.

According SENER, Mexico had 53.5 gigawatts (GW) of effective generation capacity in 2013. The country generated an estimated 258 billion kilowatthours (kWh) of electric power in 2013, representing an increase of nearly 25% from a decade ago. Fossil-fueled power plants provide most of Mexico's electricity capacity and generation. Industry accounts for 58% of Mexico's electricity sales, while the residential sector is responsible for just over one-quarter of sales.

Electricity trade between the United States and Mexico has existed since 1905, when privately-owned utilities located in remote towns on both sides of the border helped meet one another's electricity demand with a few cross-border low voltage lines. Over the years, both countries developed highly regulated and structured electricity sectors, and major and minor cross-border transmission lines were constructed. However, for a variety of technical and market reasons, U.S.-Mexico electricity trade has remained small. Existing electrical interconnections between Mexico and the United States are relatively limited in capacity and are operationally constrained by non-synchronous cross-border ties, except in the Southern California-Baja California region.

Mexico has been a modest net exporter of electricity to the United States since 2003 according to EIA. In 2012, Mexico exported a net 683 thousand kWh, representing a 16% increase from the previous year. Electricity sales from Mexico to the United States could increase in the midterm, as the U.S. Department of Energy recently issued a Presidential permit to a subsidiary of Sempra International for construction, operation, maintenance, and connection of a 230,000-volt transmission line across the U.S.-Mexico border. When completed, the transmission line will supply electricity from a Mexican wind farm to the California market. Mexico also exports smaller amounts of electricity to Belize and Guatemala.

Sector organization

The state-owned Comisión Federal de Electricidad (CFE) is the dominant player in the generation sector, controlling over three-quarters of the country's installed generating capacity. CFE also holds a monopoly on electricity transmission and distribution. In 2009, CFE absorbed the operations of Luz y Fuerza del Centro, a state-owned company that managed the distribution of electricity in Mexico City. The Comisión Reguladora de Energía (CRE) has principal regulatory oversight of the electricity sector.

The Public Electricity Service Act of 1975 established exclusive federal responsibility over the electricity industry through CFE, but amendments to Mexican law in 1992 partially opened electricity generation to the private sector. Private participation in electricity generation is now permitted in certain categories, including construction and operation of private plants for self-supply, cogeneration, small production (under 30 MW), and import/export. Any company seeking to establish private electricity generating capacity or to begin importing and/or exporting electric power must obtain a permit from CRE. As of mid-2012, independent generators—Productores Independientes de Energía (PIE)—held about 12.2 GW of generation capacity, consisting mostly of combined-cycle, gas-fired turbines.

Mexico's national transmission grid, which is operated by CFE, includes over 31,000 miles of mostly high- and medium-voltage lines. According to the CFE, over 97% of Mexico's population has access to electricity.

Fossil fuels

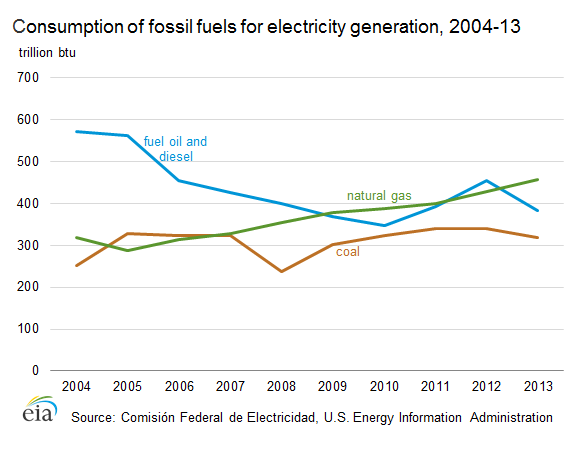

Power plants using fossil fuels comprise the overwhelming majority of Mexico's electricity generation. In the past, petroleum products were the leading fuels in Mexico's electric generation mix. However, natural gas consumed for electricity generation has risen significantly in recent years, a shift that has been a leading driver of Mexico's rising natural gas consumption. Coal consumption by the power industry has also risen in recent years.

Nuclear

Mexico has a single nuclear power plant, Laguna Verde, in Veracruz. Laguna Verde's reactors are operated by CFE, which in April 2007 awarded a contract to an international consortium headed by Alstom to modernize the plant. This modernization increased total nuclear generating capacity from 1,400 megawatts (MW) in 2007 to 1,610 MW in 2012 according to the CFE.

Renewables

Hydroelectricity supplied about 11% of Mexico's electricity generation in 2013. The largest hydroelectric plant in the country is the 2,400-MW Manuel Moreno Torres, at Chicoasén dam in Chiapas. Another major hydroelectric project, the 750-megawatt La Yesca facility, was completed in November 2012. The 900-megawatt La Parota project has been effectively cancelled because of local opposition.

Nonhydro renewables represented 3% of Mexico's electricity generation in 2013. The most significant source is currently geothermal, including the 645-MW Cerro Pietro plant in Baja California, followed by biomass and waste combusted in fossil-fueled power plants. At present, there is relatively little wind and solar generation in Mexico.

Several wind projects are in development in Baja California and southern Mexico. The Isthmus of Tehuantepec in Oaxaca has especially favorable wind resources and has been a focus of government efforts to increase wind capacity. The Oaxaca II, III, and IV wind projects came online in the first half of 2012, and are due to be joined by the Oaxaca I and La Venta III projects later in 2014 to early 2015. Each project phase includes just over 100 MW of capacity. In Baja, Sempra International is developing the Energía Sierra Juarez (ESJ) wind farm. The electricity from this farm will be exported to the United States on a new transmission line. The 156-MW first phase of ESJ will be completed in 2014. ESJ's long-term development plan includes additional phases, with a potential total capacity of over 1.2 GW. With these developments, Mexico is poised to become one of the world's fastest-growing wind energy producers.

Notes

- Data presented in the text are the most recent available as of April 24, 2014.

- Data are EIA estimates unless otherwise noted.

Sources

Associated Press

Business News Americas

CIA World Factbook

Comisión Federal de Electricidad

Comisión Nacional de Hidrocarburos

Comisión Reguladora de Energía

Deutsche Bank

Dow Jones

The Economist

Economist Intelligence Unit

IHS Global Insight

International Energy Agency

LatAmOil

Oil and Gas Journal

Offshore

PEMEX

Petroleum Economist

Pipeline and Gas Journal

Platts

Repsol-YPF

Reuters

Royal Dutch Shell

Secretaria de Energia

U.S. Department of State

U.S. Energy Information Administration

Wood Mackenzie

Sources

Afroil: Africa Oil and Gas Monitor (Newsbase)

APEX Tanker Data

BBC News

BP Statistical Review of World Energy, 2011

Brass LNG Limited

Business Monitor International

CIA World Factbook

Chevron

Economist

Energy Intelligence Group

Eni

Eurasia Group

EuroStat

ExxonMobil

FACTS Global Energy

Financial Times

Global Trade Atlas

Harvard- Nigeria: The Next Generation

IHS Cera

IHS Global Insight

International Energy Agency

International Maritime Organization

International Monetary Fund

New York Times

Nigeria LNG Limited

Oil and Gas Journal

OPEC Annual Statistical Bulletin

Petroleum Africa

Petroleum Economist

Petroleum Intelligence Weekly

PFC Energy

Reuters

Rigzone

Shell

Total

U.S. Energy Information Administration

West African Gas Pipeline Company Limited

World Bank

The Energy Consulting Group home page

|

E&P News and Information Scandinavian International and National International Energy

Agency Department of Trade and Norwegian

Petroleum Ministry of Industry

and E&P Project Information |

|---|